How Long Does Your Battery Last? Industry Overview - BYD vs Tesla

Lithium-ion batteries are viewed as pivotal to the decarbonisation of the transport sector (EVs) and also paired extensively with low-carbon power generation for greater control, given the intermittency of renewable energy generation (BESS).

Our team at IDCOOP (International Development and Cooperation) is pleased to present our 7th article, in the series of technology adoption all with the course of our famous format (3) topics of interest and (9) research pieces focusing on the global lithium battery industry and two companies — BYD and Tesla.

New York Stock Exchange

Tesla

The Stock Exchange of Hong Kong Ltd

BYD Ord Shs A

Lithium Battery Market:

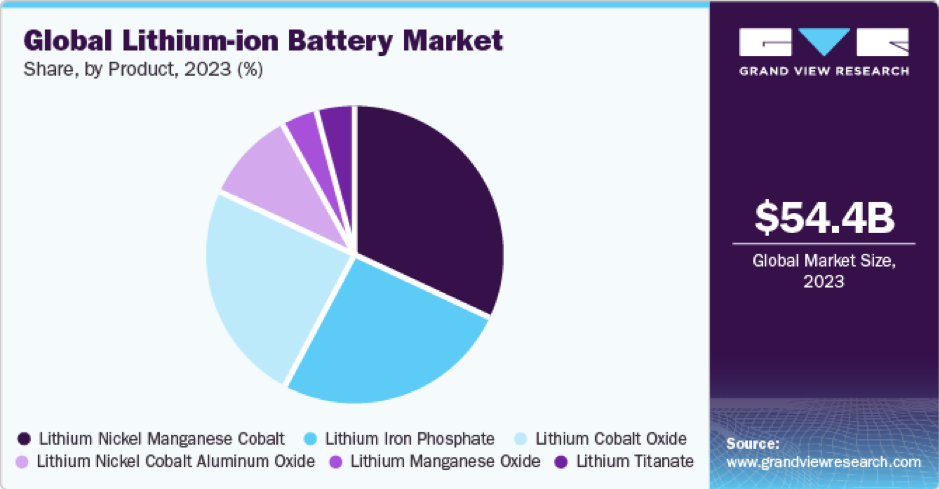

The global lithium-ion battery market size was estimated to be worth $54.4 billion in 2023 (figure 1) and is expected to increase to $182.5 billion by 2030. This growth is estimated at 20.3% of CAGR between 2024 to 2030.

Figure 1 — Lithium Battery Market (GVR)

Based on different cathodes, the industry has been segregated into specific sections, as highlighted in figure 1: Lithium Cobalt Oxide (LCO), Lithium Iron Phosphate (LFP), Lithium Nickel Cobalt Aluminium Oxide (NCA), Lithium Manganese Oxide (LMO), Lithium Titanate, and Lithium Nickel Manganese Cobalt (NMC) (Figure 1).

First, in terms of revenue, the LCO segment accounted for the largest market share of over 30.0% in 2023. High demand for LCO batteries in mobile phones, tablets, laptops, and cameras, on account of their high energy density and high safety level, is expected to augment segment growth over the forecast period.

Second, in terms of the overall dominant chemistry mix, Lithium nickel-manganese-cobalt (NMC), chemistries are the dominant battery chemistry mix so far, in part on its superior energy capacity — intrinsically linked to driving range — especially compared with the cheaper and safer lithium-iron-phosphate (LFP) batteries.

Third, LFP batteries provide excellent safety and a long-life span to product in the case of BYD’s electric vehicles and battery energy storage systems (BESS). Thus, rising demand for lithium iron phosphate batteries in portable and stationary applications is expected to augment industry growth, as they require high load currents and endurance. Especially, due to China establishing supportive policies around the adoption of technologies using LFP (EVs and energy storage systems).

Fourth, the rising demand for NCA on account of its high specific energy, specific power, and long-life span is expected to augment segment growth over the forecast period. NCA finds use in EV vehicles, medical devices, and industrial applications. In addition, Tesla vehicles are known to use several different battery cathodes, including nickel-cobalt-aluminum (NCA) cathodes and lithium-iron-phosphate (LFP) cathodes (regarding its vehicles made for the Chinese market).

Increasing consumption of lithium titanate in various applications including electric powertrains, streetlights, UPS, and solar-powered street lighting is likely to fuel segment growth over coming years. LTO offers various properties including safety, low-temperature performance, and high life-span, which is expected to increase its share over the forecast period.

Dominant Applications: EVs and Battery Energy Storage Systems

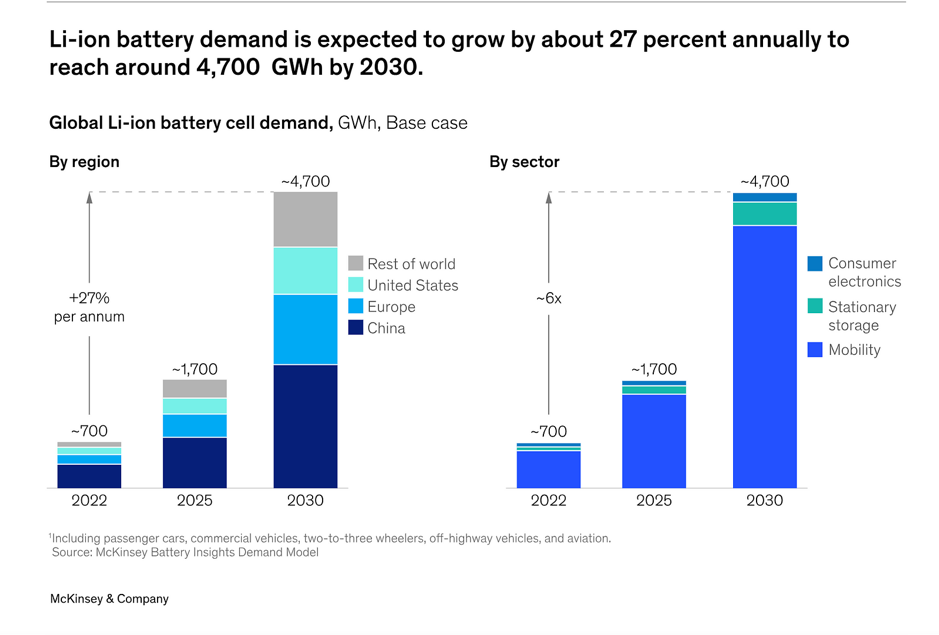

Li-ion Batteries for mobility applications, mainly electric vehicles (EVs), will account for the vast bulk of demand in 2030 — about 4,300 GWh; an unsurprising trend seeing that mobility is growing rapidly. Moreover, EVs are expected to dominate the Li-ion battery demand (Figure 2). Especially, as electric car vehicles exceeded 17 million globally in 2024, reaching a sales share of more than 20%. Just the additional 3.5 million electric cars sold in 2024 compared with the previous year is more than the total number of electric cars sold worldwide in 2020. Furthermore, in 2022, BYD’s vehicle sales raced ahead of Tesla’s and are now well more than twice as high, three times as much in Q4 2024.

Figure 2 — Sectors (McKinsey & Company)

In many markets, grid constraints mean wind and solar capacity is often curtailed during high availability, pushing wholesale prices to zero or below. Conversely, grid operators largely rely on gas plants when intermittent wind and solar are unavailable, ramping these assets quickly and driving prices to extreme highs. These economics are driving the rapid growth in BESS to expand renewable generation and optimise grids.

Battery energy storage systems (BESS) will have a CAGR of 30% (Figure 2) , and the GWh required to power these applications in 2030, will be comparable to the GWh needed for all applications today. Moreover, Battery storage costs dropped by nearly 20% in 2024, amid oversupply and an ongoing price war.

Increasing cell sizes and energy density will further push down prices. Battery container costs could potentially fall by almost 40% from US$160/kWh to below US$100/kWh by 2030, further driving demand. Combined with solar PV, which already offers a low cost of electricity, declining battery costs mean hybrid applications such as solar-plus-storage systems will become one of the lowest cost and reliable forms of electricity by 2035.

BYD and Tesla Strategy Comparisons:

Tesla’s Main Strategies :

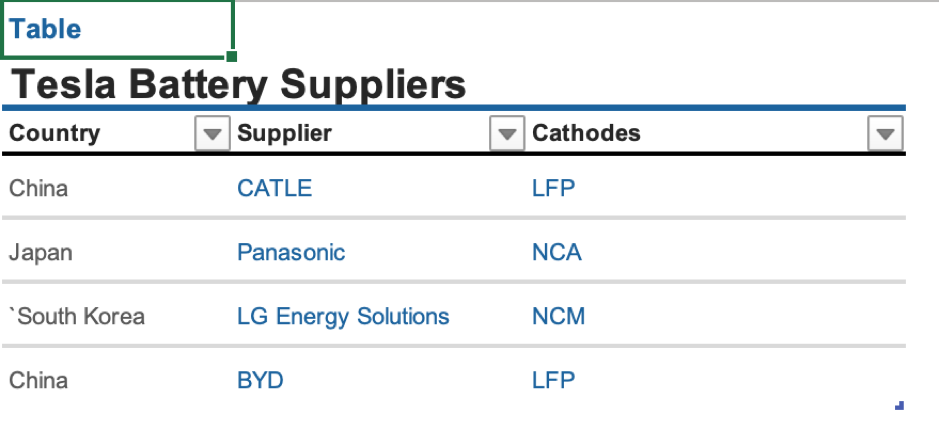

Figure 3 — Tesla’s Main Battery Suppliers (IDCOOP)

Tesla doesn’t make its own batteries, instead, the company works with multiple battery suppliers. This would include Panasonic, its long-time partner, as well as LG Energy Solutions, the second largest battery supplier in the world. They supply the EV maker with cells containing nickel and cobalt.

China’s CATL has been supplying LFP batteries to Tesla for cars made at its Shanghai plant since 2020. It’s also been reported that BYD Company (OTC Pink:BYDDF, SZSE:002594) is supplying Tesla with the Blade battery — a less bulky LFP battery — which the car manufacturer has used in some of its models in Europe.

In the case of Tesla’s battery energy storage systems (BESS), according to LatePost (via CnEVPost), BYD’s FinDreams battery unit has secured a contract for more than 20% of Tesla’s anticipated BESS manufacturing capacity in China.

The remaining 80% of batteries will likely come from CATL. In addition, BYD is set to work with Tesla on its battery energy storage systems (BESS) in China, with a plan to supply 20% of Tesla’s anticipated BESS manufacturing capacity, with CATL expected to cover 80%. The factory, which began production at the close of 2024, uses the companies’ LFP batteries.

BYD’s Approach :

In comparison to Tesla, BYD, notably, makes its own chips and batteries in- house. Alongside other vertical integrations, which helps make BYD a low-cost EV maker. Moreover, BYD’s Blade batteries is lithium iron phosphate batteries (LFP). Despite being competitors, BYD supplies Tesla and other third-party EV makers (including Xiaomi, XPeng’s Mona sub brand, Nio’s Orvo bran and Toyota) with the company’s battery technology.

Moreover, BYD now has unveiled its 1,000-kilowatt super-fast charging technology, twice the charging power of Tesla’s V4 Supercharger. It can charge at 2 miles per second, providing essentially a full charge in roughly five minutes. Fast charging is a game-changer for EV adoption, eliminating concerns about long waits and range anxiety.

Critique:

The analysis of the Lithium-ion battery industry encompasses three key areas: the global industry landscape, the primary applications leveraging lithium batteries, and a strategic comparison between Tesla and BYD. These sections provide a comprehensive overview of the industry of the industry’s current state, including its expansive market growth and the critical applications driving innovations in electric vehicles, consumer electronics and renewable energy storage systems.

Furthermore, each area highlights how the latest technological advancements, such as improved battery ranges and safety features, underscoring lithium’s essential role in reducing carbon emissions from automobiles and enhancing the stability of renewable energy grids. This mineral’s significance is magnified by ongoing developments. We must underscore the absolute different between Tesla batteries physical composition, function utility and performance, whilst comparing those with BYD products for each individual and business requirement and preference.

References:

- https://www.grandviewresearch.com/industry-analysis/lithium-ion-battery-market

- https://investingnews.com/where-does-tesla-get-lithium/

- https://www.iea.org/reports/global-ev-outlook-2025/executive-summary

- https://www.spglobal.com/market-intelligence/en/news-insights/research/lithium-ion-battery-capacity-to-grow-steadily-to-2030

- https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/battery-2030-resilient-sustainable-and-circular

- https://www.woodmac.com/blogs/the-edge/battery-energy-storage-comes-of-age/

- https://www.investors.com/news/tesla-vs-byd-ev-sales-robotaxis/

- https://www.163.com/dy/article/J3U3C0H60531M1CO.html

- https://cnevpost.com/2024/06/05/byd-findreams-to-supply-battery-cells-to-tesla-megafactory/